Table Of Content

Start your mortgage application to see what loan program you qualify for today. The loan-to-value ratio (LTV) is another factor used to determine how you qualify for a home loan. Your LTV is the loan amount divided by the home’s purchase price. There are many ways to calculate a credit score, but the most sophisticated, well-known scoring models are the FICO®Score and VantageScore® models. With nearly two decades in journalism, Dori Zinn has covered loans and other personal finance topics for the better part of her career. She loves helping people learn about money, whether that’s preparing for retirement, saving for college, crafting a budget or starting to invest.

How to improve your credit score to buy a house

It’s important to shop around and compare your options with as many mortgage lenders as possible to find a good deal. Many lenders let you get pre-qualified with only a soft credit check that won’t hurt your credit. Pre-qualification will give you a rough estimate of what you might be able to borrow from a lender, which can help you see what you can realistically afford. Research different mortgage types to gauge which one fits your situation best. For example, while conventional mortgages are the most popular type, you might qualify for better terms on a home in a rural area with a USDA loan. You could also look into programs for first-time homebuyers, if applicable.

USDA home loan requirements:

Whether you’re buying or refinancing a home, learn five steps that will help you learn how to choose the best mortgage lender for you. “Mortgage lenders will use the lowest middle FICO score of all borrowers on an application,” says Richard Simon, owner of AZ Lending Experts LLC. Uncover down payment assistance programs and down payment assistance grants that can ease the financial burden of a home purchase.

What Is a Good Credit Score? - NerdWallet

What Is a Good Credit Score?.

Posted: Fri, 12 Apr 2024 07:00:00 GMT [source]

Compare lenders and get preapproved

No down payment is required, but you’ll pay upfront and annual guarantee fees that work like FHA mortgage insurance. The USDA doesn’t set a minimum credit score, but most lenders require at least 640. Conventional lenders now require a 780 credit score or higher to qualify for the lowest mortgage interest rates, so anything above 780 is considered an excellent score to buy a house.

Most lenders use the FICO credit score system

Cardinal Financial Mortgage offers conventional loans, as well as FHA, VA, USDA loans, and will approve borrowers with a credit score as low as 550. While there is some correlation between income, debt and credit scores, having a high income isn't a requirement to have a high credit score. It can vary, but repairing a bad credit score typically takes anywhere from 3 to 6 years, sometimes less with some diligence and consistent effort. Similarly, credit-building loans hold the amount borrowed in a bank account while you make payments. When you pay off the loan successfully, you’ll get your money back, plus you’ll gain a record of on-time payments. Every time you apply for a new line of credit, lenders make a “hard inquiry" into your credit history. These inquiries can temporarily lower your credit score by a few points.

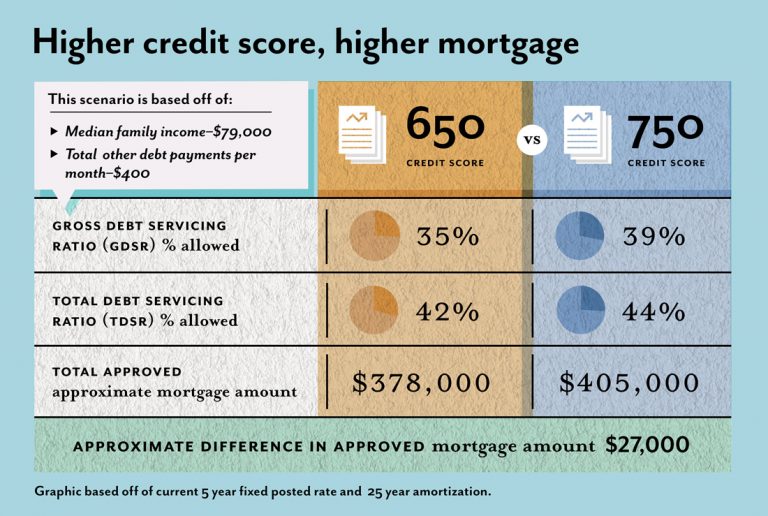

You can also get free credit reports from each of the three major credit bureaus. It’s generally a good idea to check your credit and see where you stand before you apply for a mortgage. While that may not sound like much, according to the results of that tool, the borrower with the lower credit score—Borrower A—pays $173 more every month. Prospective lenders will pull your credit score when you submit an application to assess your creditworthiness as a borrower. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether.

But getting into a home with less-than-perfect terms now can still make sense in certain situations. †The information provided is for educational purposes only and should not be construed as financial advice. Your lender may charge other fees which have not been factored in this calculation.

Conventional home loan requirements:

Most conventional loan programs will adjust your mortgage interest rate based on 20-point shifts in your credit score. So, as your credit score moves up or down 20 points, your interest rate will change accordingly, says Simon. About 90% of lenders use FICO when assessing your credit on a mortgage application. There are about 16 versions or models of the FICO score, all of which are based on a statistical analysis of your credit profile.

If your credit score is on the lower end of the spectrum, it’s smart to take steps to improve it before applying for a loan. This will unlock better interest rates and keep your costs as low as possible. To make sure your credit reports are accurate, get a free copy of your credit report from each of the credit bureaus three to six months prior to applying for a mortgage. This will alert you of any problems that could keep you from qualifying for a mortgage and give you enough time to dispute inaccuracies on your credit report with the relevant credit bureau.

Still, this score falls within the top of the fair credit score range, which means you’ll likely qualify for higher interest rates, resulting in a pricier monthly payment. Generally, the less debt you have, the better off you are when you apply for a mortgage. FICO recommends not opening new credit accounts to increase your credit utilization ratio, because each credit request can lower your score slightly.

However, in some cases, a lender may take an average of the two borrowers’ credit scores to make it easier to qualify. And a lower DTI could make it easier to qualify with your current credit score. Additionally, a more affordable home may allow you to make a larger down payment, which will reduce both your LTV and your monthly payment. Your credit score isn’t the only thing lenders consider when you apply for a mortgage. The following factors also affect your eligibility and the interest rate on your loan.

Conventional loans are the most common type of mortgage, accounting for about 70% of the market. They usually require a 620 credit score, though some lenders will consider applicants with scores as low as 580. Mortgage lenders typically want to see a score of 620 or better before approving a conventional mortgage.

For mortgages, lenders usually rely on FICO credit scoring models 2, 4 or 5. If you find errors on any of your reports, you may dispute them with the credit bureau as well as with the lender or credit card company. When it comes to your credit score, your bank or credit card issuer may provide your score for free.

Mortgage lenders generally check your FICO Score when reviewing your mortgage application. To get a broad overview of your financial situation, they’ll also pull your credit data from all three consumer credit bureaus (Experian, TransUnion and Equifax). A potential borrower with higher credit score is generally viewed as more reliable and less of a risk for lenders; the borrower with a lower credit score is seen as higher risk. A better credit score also qualifies you for a lower interest rate on your loan. Here's what minimum credit score is needed to buy a house, where to get your credit score and ways to improve your credit score quickly and efficiently. All information, including rates and fees, are accurate as of the date of publication and are updated as provided by our partners.

However, if your request to increase your credit limit is granted, it's important not to spend up to that new limit, "otherwise you'll be digging your hole even deeper," Schulz says. Rocket Homes Real Estate LLC is committed to ensuring digital accessibility for individuals with disabilities. We are continuously working to improve the accessibility of our web experience for everyone, and we welcome feedback and accommodation requests. If you wish to report an issue or seek an accommodation, please contact us at

Hopefully, this will help your credit overall—and you’ll be ready to embark on your home buying journey. And sometimes, you can even get a mortgage requiring no money down at all. Just keep in mind that no down payment can have some downsides as well. The higher your credit score, the more likely you are to both qualify for a mortgage and for one at a lower interest rate. Catch up on CNBC Select's in-depth coverage of credit cards, banking and money, and follow us on TikTok, Facebook, Instagram and Twitter to stay up to date.

No comments:

Post a Comment